Introduction

Blockchain, the technology that underpins cryptocurrencies such as Bitcoin and Ethereum, is one of the hottest topics of discussion in both business and government circles. It’s an immutable ledger that records transactions on a peer-to-peer network in real time — but what exactly does this mean for you? Well, if you’re interested in learning more about blockchain technology, I’m here to help. In this article, we’ll discuss what blockchain is and how it works so that you can understand why so many experts are calling it revolutionary.

What is Blockchain?

Blockchain is a type of digital ledger that records transactions. This technology enables the creation of a decentralized database or shared record that can be updated by multiple users in real-time.

Blockchain was originally developed as the accounting method for cryptocurrency bitcoin, but it has since grown to be used in many other applications. The technology behind blockchain allows users to make modifications to its records only if they have permission from enough participants within its network (known as “nodes”) to do so; this makes it possible for anyone with access to verify that no one has altered any information stored on the ledger without their knowledge or approval–and also makes it nearly impossible for hackers or fraudsters who gain access to manipulate data undetected because they would need access from multiple places simultaneously in order to change anything without being detected immediately by others who might notice something amiss when comparing versions at different points in time

Benefits of Blockchain Technology

Blockchain technology has many benefits. Some of the most noteworthy are:

- Decentralized – It has no central authority, so there is no single point of failure or attack. This makes it more secure and reliable than other technologies such as centralized databases where all data is stored on a single server (which can be hacked). In fact, blockchain was developed as an alternative to central banks because they were perceived as being too powerful and corruptible by their own people.

- Immutable – Since every transaction is recorded in a public ledger known as ‘blocks’, it cannot be altered without affecting all subsequent transactions on that block’s chain–and doing so would require massive computational power (or money) because everyone else would know what you did! Anyone who tries will immediately be detected by other users’ computers running mining software; they will then reject any invalid blocks from being added to their local copy of the blockchain before allowing new ones through instead.”

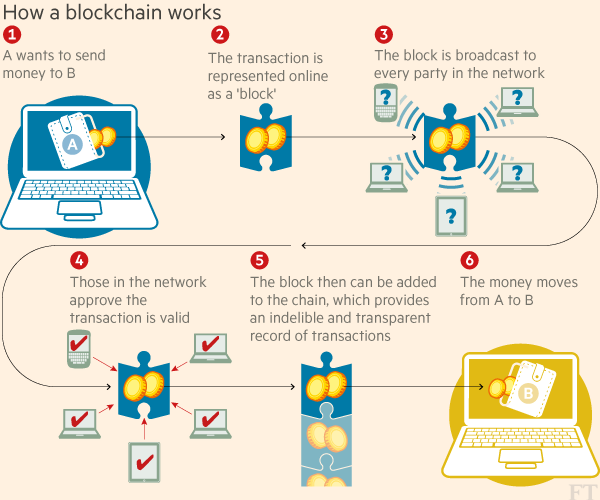

How Does Blockchain Work?

A blockchain is a distributed ledger. It’s also a type of distributed ledger, but there are many other types of ledgers that aren’t blockchains.

A blockchain is decentralized, meaning it doesn’t rely on one central authority to verify transactions or store data; instead, every node in the network maintains an identical copy of all transaction records (and stores them permanently). This makes blockchains resistant to tampering by any single party or group–no one can control them without controlling more than half of all nodes in their network at once!

Are There Any Disadvantages?

As you can see, blockchain has a lot of potential. However, it’s still a new technology and there are some disadvantages to consider:

- Blockchain is not perfect. The blockchain network is decentralized and open to anyone who wants to participate in it; however, this also means that anyone can interact with your data if they want to–which could be good or bad depending on your perspective! In other words, there may be risks involved when using blockchain technology.

- Blockchain is still evolving as more people use it for different purposes around the world every day (and night). This means there may be some bugs or errors that need fixing along the way before we get everything working perfectly smoothly all the time without any hiccups along the way… but don’t worry too much because these issues are being addressed quickly so they don’t become major problems later down line!

The blockchain technology has come a long way in the past decade.

The blockchain technology has come a long way in the past decade. It was initially used for cryptocurrencies such as Bitcoin, but it has since evolved to be used by businesses and governments across the globe.

Blockchain is an open-source technology that allows people to make transactions without the need for an intermediary like banks or other financial institutions. Transactions are stored on blocks (hence “blockchain”), which are linked together through cryptography and time stamps that prove when they were made; this makes them tamper-proof because no one can change what’s been written down without everyone else knowing about it immediately–and even then, only if they have 51 percent consensus from other blockchains participating in a network (more on this later).

Conclusion

The blockchain technology is still in its infancy, but it has the potential to change the world as we know it. It can be used for many different things, from payments and contracts to voting systems and even social networks.

More Stories

Menyongsong Masa Depan Bersama Persatuan Ahli Farmasi Indonesia (PAFI)

How Blockchain Can Reduce Regulatory Compliance Costs

What Is The Future Of Scalability For Blockchains?